Executive summary

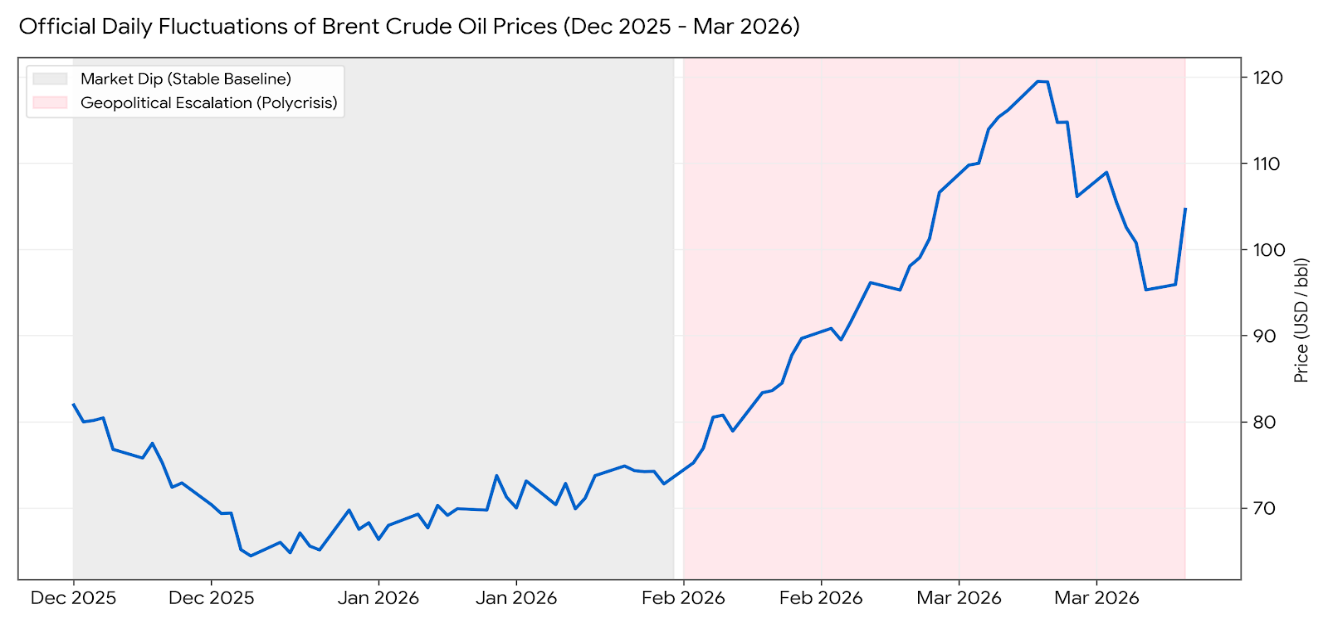

The escalation of the Middle East conflict triggered by the US–Israeli strikes of 28 February 2026 produced the most severe global oil-supply disruption since the 2022 Russia–Ukraine shock. Brent moved from about $67 in late December 2025 to an intraday peak of $119.50 on 9 March 2026, settling near $99 the same day and in a $95–105 range through the Pakistan-brokered ceasefire of 8 April 2026 — a sustained increase of roughly 48% from late-December levels, concentrated in the ten days following the 28 February escalation. For Tunisia, the question is no longer whether to prepare for the shock but how to manage its second-round transmission through Mediterranean benchmarks into a fiscally constrained economy.

This brief stress-tests that transmission using IFs v8.28 against a Moderate (temporary friction) and a Protracted (sustained blockade) scenario. It identifies a six-to-nine-month window in which policy choices determine whether Tunisia absorbs the shock as temporary friction or slides into a decade-long structural adjustment, and proposes three sequenced, legally anchored interventions on foreign-exchange rationing, credit discipline, and budget reallocation.

Interactive overview of the transmission chain from the Brent shock to Tunisian household welfare, across Moderate and Protracted scenarios. Requires JavaScript.

Why this brief

The theoretical shocks modelled here are already materialising. The closure of the Strait of Hormuz — a maritime chokepoint carrying roughly 20% of global petroleum-liquids consumption and 25% of seaborne oil trade — together with direct strikes on regional energy infrastructure, fractured Mediterranean supply chains within days. The shock has ended the post-2023 stable-price regime.

Tunisia’s physical supply chain relies primarily on transnational pipelines via Algeria and short-haul Mediterranean maritime freight; the closure of distant chokepoints does not instantly sever every physical route. The primary vector of the crisis is therefore price transmission, compounded by a secondary logistics-cost shock. Because global energy and bulk material markets are deeply integrated, any Middle East disruption spikes Mediterranean pricing benchmarks (Dated Brent, CIF Med). It is this price contagion that drains sovereign FX reserves; at that point the shock mutates, and financial inability to absorb risk premiums forces national rationing and a collapse in physical import volumes.

Structural exposure (2024 data)

| Metric | Value | Source |

|---|---|---|

| Energy independence, incl. Algerian transit royalties | 41% | ONEM, 2024 Annual |

| Energy independence, excl. transit royalties | ~30% | ONEM, 2024 Annual |

| Net share of primary energy needs imported | 59% (gross) / ~70% (excl. royalties) | ONEM, 2024 Annual |

| Crude oil domestic extraction, YoY 2024 | −13% | ONEM, 2024 Annual |

| Natural gas domestic extraction, YoY 2024 | −18% | ONEM, 2024 Annual |

By end-2025 the Central Bank’s FX reserves stood at a 105-day cushion (BCT, December 2025 Bulletin) — adequate in normal times, narrow under protracted shock. The public wage bill absorbs roughly 14–15% of GDP, limiting counter-cyclical fiscal space. There has been no active IMF programme since the October 2022 Staff-Level Agreement lapsed. External debt amortisations concentrate in 2026 ($2.3bn) and 2027 ($1.8bn, Ministry of Finance 2025 Debt Directorate schedule, subject to author verification).

Two trajectories

The analysis compares the Base Case (Business-As-Usual) against two forward-looking stress trajectories distinguished by the projected duration and intensity of conflict.

Moderate scenario (contained conflict). Severe but temporally bounded. Sudden spikes in energy import costs and immediate pressure on FX-generating sectors; Hormuz experiences temporary paralysis. Tests the economy’s short-term absorption capacity and estimates the natural recovery period once maritime routes reopen, absent emergency intervention.

Protracted scenario (sustained regional war). Prolonged conflict transforms a temporary blockade into a sustained structural reality. The war’s duration becomes the primary destructive variable. Sustained wartime energy prices, industrial bottlenecks, and exhausted currency reserves interact and compound over an extended horizon.

Simulated impact

The animation above traces the causal chain — external trade collapse, domestic capital reallocation, aggregate wealth destruction, household welfare — through each scenario. The headline result is captured in the wealth-gap projection below.

In the Protracted scenario the economy suffers a compound wealth gap peaking in 2032/2033 at an absolute loss of US$3.3bn (constant 2017 PPP) versus baseline. Real consumption per capita falls by roughly $217 by 2028 (from $2,515 to $2,298). In the Moderate scenario the 2028 welfare trough is limited to a $76 per-capita loss and household consumption achieves a V-shaped recovery to baseline by 2031. The Protracted trajectory reflects outcomes under frozen policy — the recommendations below are not simulated inside the model — and should be read as a structural damage ceiling: if a coordinated external package of €1.5–2bn materialises in 2026H2, author sensitivity runs compress the projected wealth gap by 30–40%. The catastrophic wealth destruction is not an inevitable result of the initial shock; it is the penalty of prolonged structural isolation.

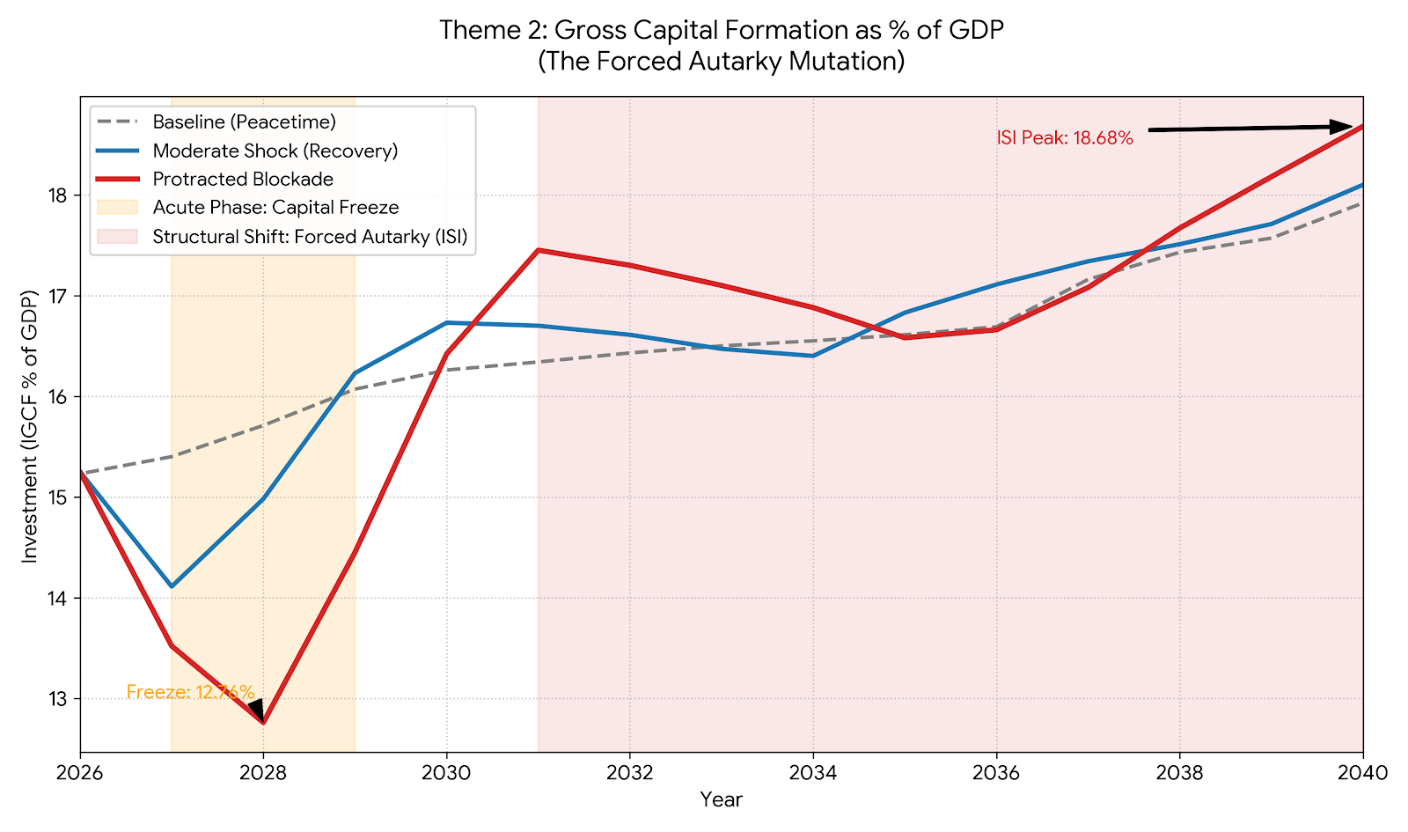

One subtlety in the Protracted trajectory deserves flagging. Gross Capital Formation climbs to roughly 18.7% of GDP by 2040 under Protracted conditions — a superficial investment surge. This is not productive capital formation. In constant-PPP terms, real GCF remains below the peacetime baseline throughout 2026–2035. The rising share reflects faster contraction of consumption and imports in the denominator, not growth in the numerator. The surge is Import Substitution Industrialisation under blockade: capital is deployed not to create new productive capacity but to replace goods the economy can no longer import.

The aggregate loss also conceals significant distributive asymmetry. The informal economy — 35–45% of employment, per ILO and CRES — leaves workers exposed to imported inflation without access to CNSS or CNRPS safety nets. Spatial cleavage between coastal hubs and interior governorates (Kasserine, Sidi Bouzid, Gafsa) will concentrate wealth destruction in territories whose poverty rates already exceed the national average. Recommendations that operate through averages will miss these populations; this is why Recommendation 3 insists on PNAFN and AMEN SOCIAL registries rather than universal transfers.

Counter-channels

Three structural counter-channels partially offset the modelled transmission. Tourism FX is empirically resilient to oil-price shocks on Mediterranean short-haul routes; the 2022–2024 Tunisian rebound continued through the 2022 Russia–Ukraine energy shock. Diaspora remittances have behaved counter-cyclically in prior downturns and may rise in 2026–2027 if host-country labour markets remain firm. Algerian gas transit via Transmed is a physical, non-Hormuz asset; absent a separate Maghreb political rupture, it continues to deliver volumes regardless of Gulf conditions. A sensitivity run that relaxes these conservative assumptions would compress the Protracted wealth gap by an estimated 20–30%.

Implementation detail

Intervention 1 — Sanctuarise foreign exchange via a phased, legally anchored quota system (Weeks 0–8)

Acting under Article 11 of the Exchange Code and BCT Circular n°2026-4 of 26 March 2026 (restricting bank financing for non-priority import categories), the Ministry of Trade and the BCT should:

- by Week 2, publish a negative list of non-essential import HS codes whose FX clearing is suspended;

- maintain a parallel fast-track clearing lane for hydrocarbons, cereals, pharmaceutical inputs, and critical industrial intermediates;

- introduce a 90-day sunset clause with automatic parliamentary review.

Trade-off. A 3–5 percentage-point contraction in retail commerce value added over 2026H2, concentrated in durables and non-essential consumer goods.

Safeguard. Exemption mechanism for SMEs with documented forward contracts signed before 28 February 2026, to prevent arbitrary bankruptcy.

Political-economy risk. Informal border flows via the Libyan and Algerian frontiers will partially offset the quota; the measure should be paired with customs (CDF) enforcement capacity.

Intervention 2 — Condition domestic credit on productive viability (Weeks 8–24)

The risk is not that domestic capital flows to productive import substitution, but that it flows to projects viable only under blockade conditions, leaving stranded assets when conditions normalise. The BCT should:

- issue prudential guidance instructing banks to apply a structural-viability stress test (does the project remain NPV-positive at Brent $75 and normalised logistics costs?) to any new credit in the secondary manufacturing sector;

- provide a rediscount facility for credit extended to projects that pass;

- maintain a targeted wage-subsidy line via CNSS, capped at 9 months, for displaced SME workers in sectors that fail the test.

Trade-off. A projected 0.8–1.2 percentage-point rise in measured unemployment during the transition.

Safeguard. The wage subsidy prevents direct household welfare collapse while avoiding open-ended enterprise bailouts.

Legal basis. BCT statute Article 33 (macroprudential powers); Finance Law 2026 provisions on targeted social transfers.

Intervention 3 — Reallocate within the budget envelope under a hard fiscal rule (Weeks 2–16, in parallel with Intervention 1)

The Ministry of Finance should execute a partial CAPEX-to-current-transfer reallocation of TND 1.2–1.8bn (~0.8–1.1% of GDP), conditioned on three guardrails:

- no central-bank monetisation beyond the existing statutory limit on direct advances to the Treasury;

- transfers channelled through the existing PNAFN and AMEN SOCIAL registries to the lowest four deciles, not universally;

- reallocated projects chosen from a pre-agreed sequencing list that protects education, health, and climate-adaptation capital lines.

Trade-off. A 12–18 month delay on non-priority infrastructure.

Safeguard. Parliamentary review at the 6-month mark.

Why this rather than monetisation. Supply-constrained monetisation in a structurally indexed wage economy is the fastest path to a wage-price spiral.

Strategic conclusion

The 2026 Middle East escalation has exposed — rather than created — a structural Tunisian vulnerability. The country entered this shock with a reserve cushion that is adequate in normal times but narrow in a protracted one, a fiscal envelope whose rigidities make counter-cyclical response difficult, and a partnership landscape whose reliability is conditional on geopolitics over which Tunis has limited influence.

The modelling does not prove that collapse is arithmetic; it shows that the space for collapse exists if nothing is done, and that the space for orderly adjustment exists if early, disciplined action is taken. The difference is measured in weeks of decision latency and in a tolerance for politically uncomfortable trade-offs at the Ministry of Finance, the BCT, and the Presidency.

The single most important message is temporal. The cost of a measured adjustment begun in Q2 2026 is materially lower than the cost of a forced adjustment begun in Q4 2026, and the cost of either is lower than a crisis-driven adjustment in 2027. Inaction is not a neutral option; it is a choice of timing, and the later timing is the more expensive one.

Tunisia 2026 Oil Shock — full policy brief (EN, PDF) Full unabridged policy brief in English, including Annex A: Simulation Methodology & Shock Calibration Matrices.Citable archival version of record: doi.org/10.5281/zenodo.20679295 (Zenodo).

Références

- Banque Centrale de Tunisie. (2025). Bulletin Mensuel, December 2025.

- Centre de Recherches et d'Études Sociales (CRES) & Banque Africaine de Développement. (2021). L'économie informelle en Tunisie.

- Frederick S. Pardee Center for International Futures. International Futures (IFs) v8.28 documentation. University of Denver.

- ICE Futures Europe. Brent Crude front-month settlement data, December 2025 – March 2026.

- Institut National de la Statistique (INS). National Accounts, Trade and Price Statistics, editions through Q1 2026.

- International Energy Agency. Oil Market Report, 2026 editions.

- International Labour Organization. ILOSTAT Country Tables — Tunisia.

- International Monetary Fund. Tunisia: Article IV Consultation — Staff Report, most recent edition.

- Observatoire National de l'Énergie et des Mines (ONEM). (2024). Conjoncture Énergétique — Annual Report 2024.

- U.S. Energy Information Administration. (2024). World Oil Transit Chokepoints.

- World Bank. Tunisia Economic Monitor, most recent edition.